Article

Master Sergeant Gannon Ken Van Dyke used classified information about Operation Absolute Resolve to profit from prediction markets. Harvard researchers flagged $143 million in suspected insider profits. The data signatures were visible all along. Here's what they look like — and why the industry's integrity infrastructure isn't ready.

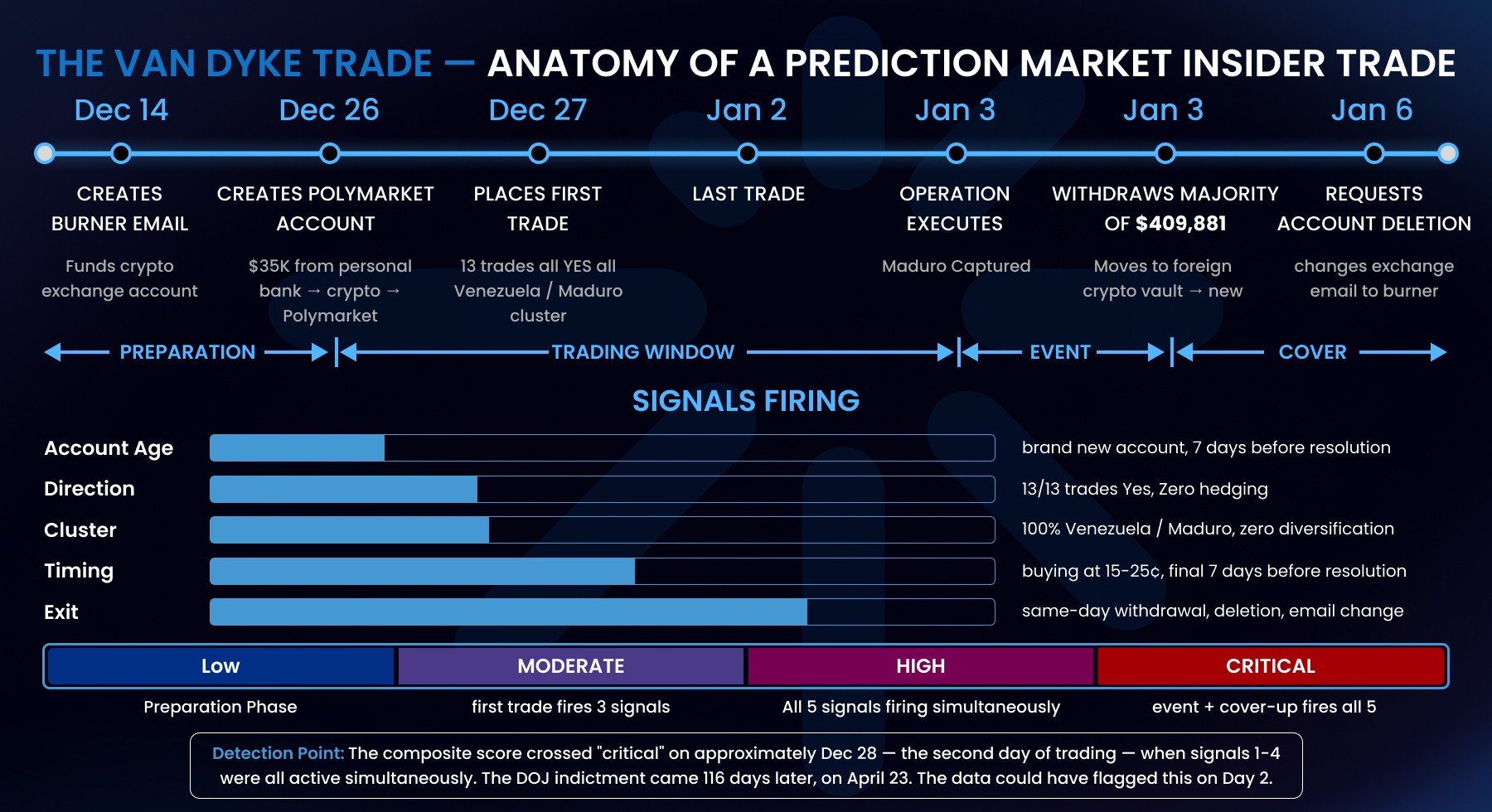

On the evening of January 2, 2026, a few hours before U.S. Special Forces flew into Caracas to capture Venezuelan President Nicolás Maduro, a soldier named Gannon Ken Van Dyke allegedly placed his final bets on Polymarket.

He had helped plan the operation. He had signed nondisclosure agreements. He knew, in precise operational detail, what was about to happen. And between December 27 and January 2, he placed 13 bets — all YES positions — on contracts including "US Forces in Venezuela by January 31," "Maduro out by January 31," and "Trump invokes War Powers against Venezuela by January 31."

His total investment: approximately $33,000. His total profit: $409,881.

On April 23, 2026, the Department of Justice unsealed the indictment. The CFTC filed a parallel civil complaint. It is the first criminal prosecution for insider trading on a prediction market in United States history.

But Van Dyke's trades were not invisible before the FBI got involved. They had a data signature. And that signature was detectable — algorithmically, in real time — long before Polymarket's compliance team referred the matter to the DOJ.

This is the story of what insider trading looks like in prediction market data, why the industry's integrity tools aren't ready for the scale of the problem, and what it would take to fix it.

The Pattern

Van Dyke's trades had five characteristics that, in combination, form a recognizable signature:

New account. The Polymarket account was created on December 26, 2025 — one week before the operation. No prior trading history. No established pattern. A fresh wallet funded with approximately $35,000 from a personal bank account via a cryptocurrency exchange.

Single-direction concentration. All 13 trades were YES positions. No hedging. No portfolio diversification. No bets on unrelated markets. Every dollar went in one direction on one cluster of contracts.

Narrow contract cluster. The bets targeted a tight group of related contracts — all involving Venezuela, Maduro, or U.S. military action. A legitimate trader with a geopolitical thesis might spread across Iran, Venezuela, and election markets. Van Dyke bet exclusively on the operation he was helping to plan.

Pre-event timing. The trades were placed in the final week before resolution, when the contracts were still priced as uncertain. By the time Van Dyke began trading, the market implied roughly 15-25% probability for most of the contracts he bought. He was buying cheap contracts that he knew would resolve to $1.

Immediate post-resolution exit. On the day of the operation, Van Dyke withdrew the majority of his winnings. He then asked Polymarket to delete his account, falsely claiming he had lost access to his email address. He changed the email on his cryptocurrency exchange to a burner address he had created weeks earlier.

Each of these signals alone is common. New accounts are created every day. Single-direction bets happen in every market. Narrow cluster trading is normal for anyone following a specific news story. Pre-event timing is how markets are supposed to work. And withdrawals happen after every resolution.

Table 1: "The Insider Trading Signature: Five Signals That Flag Anomalous Prediction Market Trades"

Signal | What It Measures | Van Dyke's Pattern | Normal Trader Baseline | Detection Threshold |

|---|---|---|---|---|

Account Age | How new is the wallet relative to the trade? | Created Dec 26 — 7 days before resolution | Median account age at trade: 47 days | Trade within 14 days of account creation on a high-value contract |

Directional Concentration | What percentage of trades are single-direction (all YES or all NO)? | 100% YES — 13 out of 13 trades | Typical trader: 60-70% single direction across portfolio | >95% single direction AND >$10K total position |

Contract Cluster Density | How narrowly are trades concentrated in related contracts? | 100% in Venezuela/Maduro cluster — zero diversification | Typical trader: 3-5 unrelated categories | >80% of positions in contracts sharing the same underlying event |

Pre-Resolution Timing | How close to resolution were the trades placed? | Final 7 days before operation — buying at 15-25¢ | Typical position: entered 14-30 days before resolution | >50% of position entered within 7 days of resolution at odds below 30¢ |

Exit Velocity | How quickly did the trader withdraw after resolution? | Same-day withdrawal + account deletion request + email change to burner | Typical winner: reinvests 40-60% of profits into new positions | Full withdrawal within 24 hours of resolution + no subsequent trades |

Any single signal: common. Two signals combined: notable. Three or more: statistically anomalous. All five: the Van Dyke pattern.

The Harvard study used a similar composite methodology across 93,000 markets and found 210,718 suspicious wallet-market pairs. The five-signal framework isn't theoretical — it's been validated against two years of on-chain data.

But in combination — and especially when scored against baseline trading behavior across tens of thousands of wallets — the pattern is statistically extraordinary.

The $143 Million Problem

Van Dyke is not an isolated case. He's the first prosecution in a pattern that Harvard researchers have now quantified.

In March 2026, researchers at Harvard Law School published a study analyzing public blockchain data across 93,000 Polymarket markets and nearly 50,000 unique wallet addresses from February 2024 through February 2026. They developed a composite scoring system combining five signals: cross-sectional bet size, within-trader bet size, profitability, pre-event timing, and directional concentration.

Their finding: across 210,718 suspicious wallet-market pairs, flagged traders achieved a 69.9% win rate — a result that exceeds random chance by more than 60 standard deviations. The estimated aggregate anomalous profit: $143 million.

A separate study by researchers from London Business School and Yale University, analyzing 1.72 million accounts and $13.76 billion in trading volume from 2023 to 2025, found that approximately 3% of accounts — "expert winners" — captured over 30% of all profits. The study flagged 1,950 accounts for suspected insider trading.

These are not conspiracy theories. They're peer-reviewed statistical analyses using publicly available on-chain data. And the cases keep multiplying:

"Magamyman" — an account that placed its first trade 71 minutes before news of the U.S.-Israeli strike on Iran broke, when markets implied only 17% probability. Profit: approximately $553,000.

The Biden pardon trader — one account correctly bet on five specific last-minute presidential pardons as the odds dropped toward zero. Profit: $316,346.

The Iran ceasefire accounts — at least 50 brand-new accounts placed substantial bets on a U.S.-Iran ceasefire hours, even minutes, before Trump announced it. Collective profit: approximately $550,000.

Two individuals in Israel, including a military reservist, arrested for placing Iran-related bets using classified information.

Three congressional candidates suspended by Kalshi for betting on the results of their own elections.

And now Van Dyke — the first criminal indictment, but almost certainly not the last.

Table 2: "The Insider Trading Timeline: Known and Suspected Cases on Prediction Markets (2025-2026)"

Date | Event | Trader | Investment | Profit | Platform | Signals Present | Outcome |

|---|---|---|---|---|---|---|---|

Jan 2026 | Maduro capture (Operation Absolute Resolve) | Gannon Ken Van Dyke (US Army Special Forces) | $33,000 | $409,881 | Polymarket (offshore) | All 5: new account, 100% YES, Venezuela cluster only, 7-day window, same-day exit + deletion | DOJ indictment — first criminal prosecution for PM insider trading |

Jan 2026 | Biden last-minute pardons (Hunter Biden + 4 others) | Anonymous (wallet linked via Bubblemaps) | ~$40,000 est. | $316,346 | Polymarket (offshore) | 4 of 5: single direction, narrow cluster (5 pardon contracts), pre-event timing (final hours), rapid exit | Under investigation |

Feb 2026 | U.S.-Israeli strike on Iran | "Magamyman" + 5 new wallets | Unknown | ~$1.2M combined ($553K Magamyman alone) | Polymarket (offshore) | 4 of 5: new accounts, single direction, Iran cluster, first trade 71 min before news at 17% odds | Under investigation — flagged by Harvard study |

Mar 2026 | Taylor Swift engagement announcement | Anonymous | Unknown | Flagged in Harvard study | Polymarket (offshore) | 3+ signals: pre-event timing, directional concentration, profitability anomaly | Flagged by Harvard — no prosecution |

Mar 2026 | Nobel Peace Prize outcome | Anonymous | Unknown | Flagged in Harvard study | Polymarket (offshore) | 3+ signals: pre-event timing, directional concentration | Flagged by Harvard — no prosecution |

Apr 2026 | U.S.-Iran ceasefire announcement | ~50 new accounts | Unknown | ~$550,000 collective | Polymarket (offshore) | 4 of 5: brand-new accounts (hours old), 100% YES on ceasefire, bets placed minutes before Trump announcement, immediate exit | Congressional investigation demanded — bipartisan |

Apr 2026 | Iran-related war bets (various) | 2 individuals incl. military reservist | Unknown | Unknown | Polymarket (offshore) | Multiple signals | Arrested by Israeli authorities |

Apr 2026 | Congressional election outcomes | 3 candidates (unnamed) | Unknown | Unknown | Kalshi (regulated) | Structural: betting on own race = definitional insider trading | Suspended by Kalshi — no criminal referral |

The pattern: Every major geopolitical event involving classified U.S. government information has generated suspicious trading activity on prediction markets. The platform of choice is overwhelmingly Polymarket's offshore exchange — the venue with the fewest surveillance obligations.

The Regulatory Gap

Here is the structural problem: the agency responsible for policing prediction markets is shrinking while the markets are exploding.

The CFTC's workforce has dropped 24% since Trump returned to office — to 535 staff, its smallest size in 15 years. Acting Chairman Brian Quintenz requested $410 million and 650 full-time positions from Congress. Even if granted, the CFTC would still be smaller than during most of Trump's first term.

Meanwhile, prediction market volume has surged to an estimated $240 billion for 2026 — a 370% increase over 2025. Bernstein projects $1 trillion in annual volume by the start of the next decade. Bank of America calls Kalshi one of the "fastest growing non-AI companies" in the U.S.

The current regulatory model relies primarily on platform self-regulation. Kalshi operates as a CFTC-designated contract market with anti-fraud and surveillance obligations. Polymarket's offshore protocol exists in a legal gray area — the same platform where Van Dyke, Magamyman, the ceasefire accounts, and the Iran strike traders all operated.

Polymarket says "the system works" because they referred Van Dyke to the DOJ. But the Harvard researchers found $143 million in suspected insider profits across 210,718 suspicious trading instances. One referral out of 210,718 is not a system that works. It's a system that caught one soldier and missed everything else.

Senator Richard Blumenthal called Polymarket "an illicit market to sell and exploit national security secrets unlike any in history, and by extension a potential honeypot for foreign intelligence services." Republican Congressman Blake Moore added: "We don't want to imagine a world where America's adversaries use prediction markets to anticipate our next move."

The Council on Foreign Relations published an essay this week calling prediction markets "an unprecedented incentive for national security insiders to leak classified information" and warning that they are "uniquely transparent venues for adversaries to exploit those leaks."

Two bipartisan bills are pending in Congress — one in the House, one in the Senate — that would broaden the definition of insider trading to cover prediction markets and tighten surveillance obligations.

What the Data Can See

Here's what makes this relevant beyond politics and regulation.

DETECTION POINT: The composite score crossed "critical"

on approximately Dec 28 — the second day of trading —

when signals 1-4 were all active simultaneously.

The DOJ indictment came 116 days later, on April 23.

The data could have flagged this on Day 2.

The Harvard researchers used five signals to identify suspicious trading: bet size relative to market, bet size relative to the trader's own history, profitability, pre-event timing, and directional concentration. They ran this analysis across two years of public blockchain data and found $143 million in anomalous profits with statistical certainty exceeding 60 standard deviations.

They did this with publicly available on-chain data.

Now consider what becomes possible with deeper data. With structured on-chain data — decoded order fills, token transfers, position splits, wallet histories — scored in real time rather than retrospectively, the detection signature becomes sharper and faster. Volume-price mismatch analysis can flag when a market moves without corresponding news. Wallet clustering can identify when "50 new accounts" are actually one entity operating through proxy wallets. Cross-venue pattern matching can detect when the same trading pattern appears simultaneously on Polymarket and Kalshi — or when it appears on one platform but not the other, suggesting the trader is deliberately choosing the less-regulated venue.

The five characteristics of Van Dyke's trades — new account, single-direction concentration, narrow contract cluster, pre-event timing, immediate exit — are all quantifiable, scorable, and detectable algorithmically. The Harvard study proved this retrospectively. The question is whether the industry builds the infrastructure to do it prospectively.

Right now, it hasn't. Platform self-regulation means each exchange monitors only its own data. No cross-venue surveillance exists. No independent data layer scores wallet behavior across platforms. No real-time anomaly detection system operates at the scale of 74,000+ active markets and $6.5 billion in weekly volume.

The intelligence layer isn't just for traders. It's for integrity.

What This Means for the Industry

The Van Dyke indictment is a watershed moment — but not because of one soldier's $400K profit. It's a watershed because it proves three things simultaneously:

One: Prediction markets have crossed from financial curiosity into national security concern. When the Council on Foreign Relations, the DOJ, the CFTC, CNN, PBS, NPR, and both parties in Congress are all focused on the same problem in the same week, the industry has entered a new phase. The regulatory and surveillance infrastructure needs to match.

Two: The data to detect insider trading already exists — on-chain, in public. Harvard proved it with a retrospective analysis. The gap isn't data availability. It's data infrastructure — the tools to process, score, and flag anomalies in real time across venues rather than months after the fact.

Three: Platform self-regulation is structurally insufficient. One caught referral out of $143 million in suspected insider profits is not a system that works. Cross-venue, independent surveillance — the same principle that underpins FINRA for stock markets and the Financial Conduct Authority for UK markets — is what prediction markets need. And it requires exactly the data infrastructure, cross-platform normalization, and analytical depth that the intelligence layer provides.

The prediction market industry is at an inflection point. It can build the integrity infrastructure before regulators build it for them, or it can wait until the next indictment — which, given the pattern of suspicious trades, won't be long.

The data is there. The signal is there. The infrastructure to read it at scale isn't.

Yet.

This is the tenth installment in the Assymetrix Intelligence Brief series.

Assymetrix is building the intelligence and synthesis layer for prediction markets — cross-platform data infrastructure for traders, builders, researchers, and the integrity systems this industry needs.

Other Blog